5 Signs Your Finance Team Is Not Audit-Ready (And What to Do About It)

You have been leading the finance team at your organization and have done an excellent job. But when the auditors asked for the six-month-old report, you were searching for it. This often happens when you ignore the signs of poor audit readiness.

According to the World Bank Enterprise Survey 2022, which surveyed 9,024 Indian MSMEs, businesses have incorporated both digital finance and records management practices.

This highlights the issue across all Indian companies. When financial records are stored in multiple places, including spreadsheets, emails, and physical file folders, preparing for audits takes longer and is more stressful.

Many Finance leaders from Bangalore’s IT and SaaS sectors, as well as from the manufacturing and business support sectors, are dealing with the CFO burnout audit during the annual checking process.

As outlined in Deloitte India’s Internal Financial Controls Survey, reliance on manual processes and paper records complicates audits and increases the time required to respond to auditor inquiries.

Audit pressure usually does not come from the audit itself. But it arises from issues that have been quietly growing throughout the year. And it gets noticed only when the auditor asks a challenging question.

This is why audit readiness is important. It helps you maintain a functional review of your finances, rather than having to run through an emergency fire drill. According to EY, audit committees expect finance teams to have more controls, enhanced documentation, and a more proactive approach to risk management.

Through this blog, lets understand what the signals are that will separate your organization from a business that is not audit-ready. Building audit readiness often requires a combination of audit support, internal controls, risk advisory, and compliance expertise. Organizations looking to strengthen these capabilities can explore SGGK’s full range of professional services

What is The Meaning of Audit Readiness?

Audit readiness means that a business’s finance team can provide complete and accurate financial records. It is achieved through consistent, timely preparation of all financial documentation requirements and by addressing any documentation gaps, which helps in preventing later disruptions to business operations.

It is not a one-time activity that occurs just before an annual audit. It is an ongoing effort requiring continuous monitoring, evaluation, and maintenance.

Why Many Companies Misunderstand Audit Readiness

Many businesses and organizations misunderstand how to maintain audit readiness. A common misconception is that businesses complete their audit prep immediately before the annual audit. This keeps them away from stress and helps them make fewer mistakes.

Businesses that undergo a smooth, efficient audit often do not have the largest teams or the most funding. These businesses keep their financial records, documentation, reconciliations, and internal controls up to date, so that they don’t have to hustle during the annual audit.

According to Deloitte India’s Internal Financial Controls Survey Report, Audit readiness in India is a continuous financial process that occurs throughout the year. Many organizations, however, view audit readiness as a pre-audit project.

A backlog of reconciliations, a lack of supporting documentation, and a last-minute hustle to complete audits are common outcomes. Organizations that achieve high levels of performance incorporate audit readiness into their month-end close processes, making the audit season a validation rather than a recovery.

Signs That the Finance Team Is Not Audit-Ready

Sign 1: Reconciliations Are Always Behind Schedule

What It Appears To Be

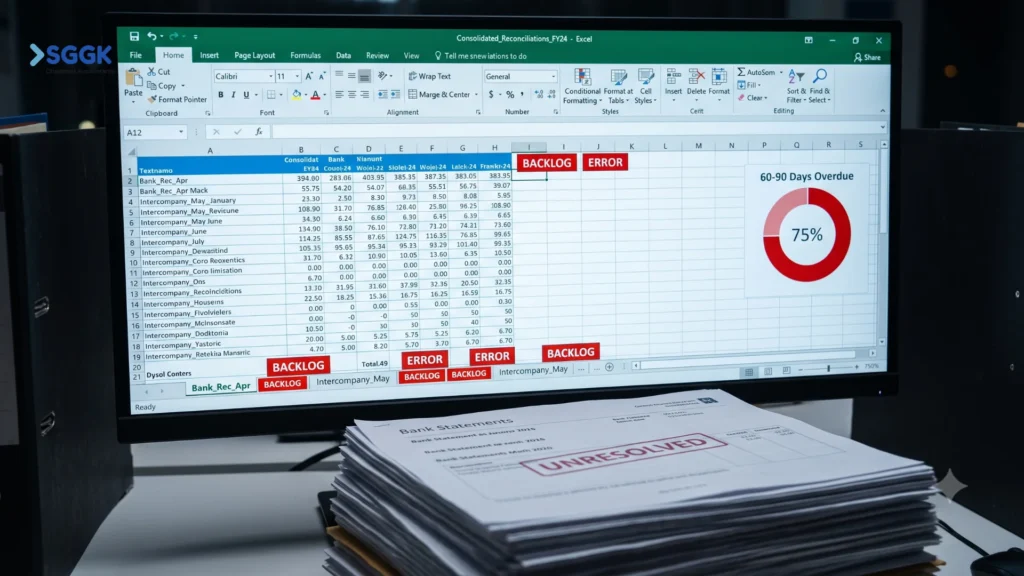

A reconciliation backlog is a warning sign that an organization is not ready for an audit. The backlog usually develops over time, making it hard for the company to identify. The month-end reconciliation cannot be completed in the same calendar month. Thus, the reconciled amounts from the previous month continue to be included in the next month.

It is very common for unresolved issues to remain untouched for 60-90 days. Multiple team members are using their own Excel files to track their progress, making it difficult to determine which file is correct or whether there are discrepancies.

Why This Creates Audit Risks?

Auditors may not know if account balances are accurate when reconciliations are missing or are late. When this happens, auditors will frequently perform the testing in more detail. They often test large samples and ask many follow-up questions.

This can slow the audit because accounting teams cannot complete certain parts until the reconciliations are finalized and confirmed.

According to a PwC report, monthly reconciliation delays result not only from the legal complexity of companies’ accounts in India but also from the nature of spreadsheets used across many departments. Manual processes for performing reconciliation quickly become a monthly audit problem.

What We Find Practical?

In the experience of numerous mid-sized companies in manufacturing and SaaS, finance departments often feel that their reconciliations are largely complete before the start of the audit season. When auditors begin their audits, they commonly see the same unexplained items that were on statements from the previous quarters.

The result is that an audit with a normal completion time of only a few weeks can stretch over several months. This results from auditors spending too much time checking for missing items from prior periods rather than working on the current year’s balances and transactions.

How SGGK Can Assist ?

SGGK assists organizations in preparing for audits by auditing reconciliation processes, assessing the financial closing cycle, and enhancing internal controls, through its Audit Support Services. Improvements made during this process help create a more efficient and predictable closing process. Also evaluate the key issues and help management in addressing those key issues which could be a show stopper during the audit. Then your teams will be ready in advance of any audit fieldwork.

Sign 2: Auditors Keep Asking for Documents You Can't Find Quickly

Poor Documentation Creates Hidden Costs

Sometimes the transactions are being recorded properly, but the related accounting documents are difficult to retrieve, insufficient to support the transactions, or scattered across various locations.

This results in missing or incomplete approval and audit delays in India. It gets difficult to retrieve contracts for an audit that an auditor requests.

What’s the problem for auditors?

While auditors require that all transactions have been accurately recorded, they also require proof that the transaction was recorded using appropriate internal control processes.

If documents are not readily accessible to an auditor or are missing components, an auditor may consider this an internal control deficiency. Properly documented material provides strong evidence that a process was applied and approved as intended.

What the auditors expect from any company is that it will provide accurate information and be able to verify the information with little or no difficulty.

According to KPMG’s Internal Control Over Financial Reporting, finance leaders often view documentation as an administrative function. But auditors do not share the same opinion.

Documentation serves as proof. If audit trails cannot be recreated in a timely manner, auditors may question the effectiveness of the processes. They don’t simply question the evidence associated with the transaction.

How SGGK Helps in Improving Your Documentation?

There are many ways companies can work to reduce the likelihood of audit-related challenges. SGGK uses a central storage system for all the documentation and supporting evidence. They ensure that documentation standards are met and identify the purpose of each transaction type. SGGK focuses on using system-based approvals and digital signatures.

The Auditing Standard 230 in India establishes how the auditor must do audit documentation. This establishes the primary evidence that the audit was planned and performed in accordance with the Standards.

Sign 3: The Same Audit Findings Appear Year After Year

What Repeat Findings Mean

The underlying cause of the repeated finding was likely not addressed. Instead, a temporary band-aid solution was implemented. There also may have been no clear assignment of responsibility to anyone in management to address the issue, nor might there be a formal tracking system to determine whether the corrective action put in place was effective.

Finance leaders may be surprised by the amount of focus auditors place on repeat findings from prior-year audits, which may indicate a lack of commitment by an organization’s management to resolving identified issues.

If the same issue is recurring from previous years, it means one is missing ownership, accountability, or a means of monitoring, rather than the finance team failing to catch a correction.

As published by ET CFO, the ICAI’s Financial Reporting Review Board published hundreds of serious complaints about audit and financial reporting non-compliance.

Preventing Recurrence of Findings

The most important thing you can do to prevent recurrence of findings is to work on completely fixing the reason for the finding, rather than only identifying the reason.

- Each finding should have a person assigned to it, with a resolution date.

- Have a remediation status update dashboard that regularly tracks progress.

- Management should perform remediation status reviews at least quarterly, not just before the next audit.

How SGGK Helps ?

We focus on both internal audits and control reviews to eliminate the root cause that led to the finding, not just fix the finding that an auditor has identified for you. Keeping the issues from reappearing in another year’s audit observations management letter. We fix the problematic root causes.

Sign 4: Your Finance Team Is Stretched Every Audit Season

Staff members consistently work long hours to complete the audit during the annual audit season. As a result, many other projects are put on hold until the audit is completed, and the finance team is stretched during the audit season.

The Human Component of Audit Preparedness

Some finance departments are efficient, yet the underlying issue of audit preparedness is often addressed by relying on a handful of individuals. When the only way for an audit to succeed is for the few employees who handle it to work long hours.

Industry Outlook: Many more firms are beginning to understand the influence of staff conscience and capacity on the quality of audit performance and the accuracy of financial reporting. It is increasingly considered unacceptable for a workforce to be under considerable stress, as this poses both financial and governance risks.

How SGGK Helps ?

They help you develop an audit calendar to schedule out key items in advance. They suggest that you perform interim reviews during the year so that you don’t face any problems later.

Plan your resources. For example, arrange for temporary or outside support when needed. Automate repetitive and time-consuming tasks such as reconciling accounts or preparing documentation. Prepare for audits throughout the year rather than waiting until the audit season.

Distributing the workload reduces stress on individuals and teams, improves documentation quality, and helps them avoid completing key items at the last minute under tight deadlines.

Sign 5: Your Financial Close Process Feels Reactive, Not Predictable

Why the Financial Close is Where Audit Readiness Begins

The primary reason is that many issues that lead to audit problems originate from a poorly performing financial close function. When month-end activities are rushed and poorly executed, there are frequent issues such as reconciliation backlogs, documentation gaps, and repeat audit findings.

A recent study conducted by OneStream has shown that to measure important close metrics, such as days to close, reconciliation backlog, or errors, you must use a structured process for measuring close metrics. Poorly performing close processes cause errors.

What SGGK suggests:

- Review the closing procedure each month to see where time is wasted.

- Track key metrics to determine how much time is being used.

- How much backlog exists, and how many changes have been made.

- Periodically test the internal controls to ensure they function as intended in actual operation and are not merely theoretical.

- Conduct multiple readiness reviews during the entire year rather than relying on a single, one-time, pre-audit exercise.

A well-organized and efficient financial closing process in India results in faster, simpler audits with fewer errors and lower compliance risks.

The Economic Times reported that Indian regulators and other professional bodies are raising the bar on audit quality and documentation standards. The finance leaders are now being held to those standards throughout the year and not just at year-end.

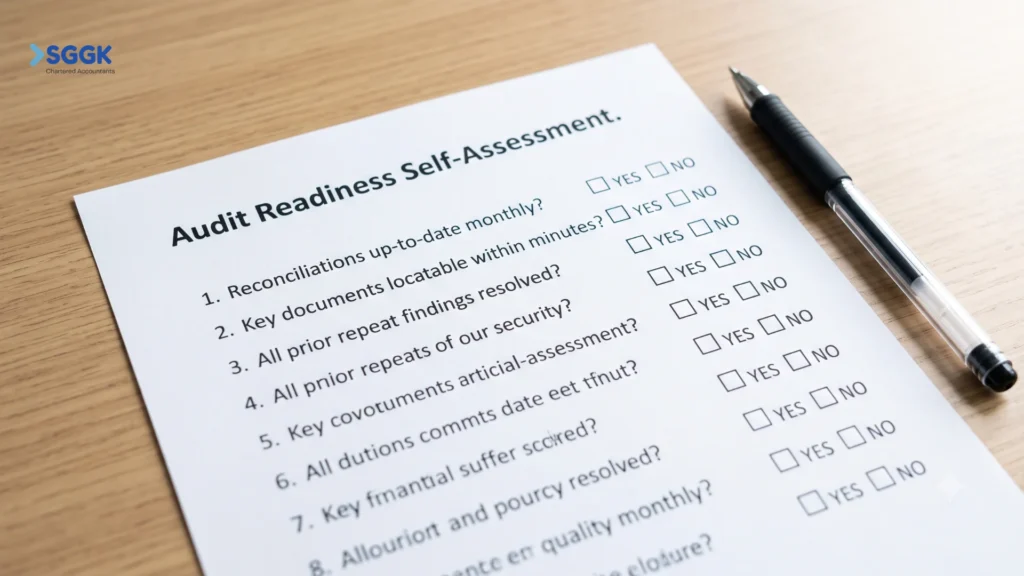

The Audit Readiness Self-Assessment Checklist

To make sure you have not missed signs of poor audit readiness. You must answer these questions for yourself as a self-assessment checklist.

- Do you complete your reconciliations every month and not carry your work into the next month?

- Can you locate key documents within minutes rather than spending hours or days searching?

- Are all prior repeat audit findings fully resolved?

- Do you also create audit pressure on your finance team?

- Do you have a consistent process for closing out each month?

- Does each task have an individual assigned to it, rather than just a department?

- Does everyone use the same documentation formatting and process?

- Do you review your files before going into the audit?

- Are all audit requests tracked in one location, and are there clear owners and status updates?

- Do you have a written audit readiness plan, rather than just preparing when you find out about an audit?

If you answered No to three or more of these questions, audit readiness should be a priority, not something you have to deal with only when it’s time for an audit.

Conclusion

It’s unusual for all of the warning signals to occur at once. Generally, they grow steadily. Account reconciliations aren’t in sync, audit observations go unaddressed, and financial staff work late to keep everything moving.

But you can identify and address these problems before the next audit. SGGK will help you identify process inadequacies and implement practical solutions to improve efficiency. They will strengthen your control environment by working with you on workflows and defining clear roles and responsibilities to help you build a strong compliance foundation.

Contact SGGK today to understand how an independent audit readiness assessment will help you achieve consistent audits, reduce stress around the time of the audit, and improve your financial results.