Internal Audit vs Statutory Audit: Key Differences Every CFO in India Must Know

Many organizations enter their statutory audit with a plan in place. But time and time again, we see organizations caught off guard by new and unexpected audit requirements, limited documentation, and compliance gaps or undisclosed items. As a result, the audit process, which should be routine, becomes a long, difficult experience for the organization.

This is prevalent among new companies, IT companies, and manufacturers in India. Internal and external audits are both methods used to evaluate an entity’s financial and operational compliance. Yet they have different purposes.

CFOs can use their understanding of the key differences between the two types of audits to guide how they will be managed, how to avoid statutory audit surprises, and to help ensure they are audit-ready all year.

In this article, we will discuss internal audit vs. statutory audit and explain how combining internal and statutory audits can create a stronger control environment for an organization’s financial processes.

Why Finance Leaders Often Confuse Internal Audit and Statutory Audit?

The Common Misconception We See During Audit Readiness Reviews

Many organizations believe that if their statutory audit has been completed successfully, they have a strong internal control system. In fact, these two concepts are very different.

The majority of companies that SGGK works with have this misconception. Generally, statutory auditors test only whether the amounts reported in the financial statements are correct and do not test day-to-day procedures in areas such as procurement, vendor management, IT access, and inventory control. This is where a structured internal audit checklist becomes critical to identifying control gaps before they become compliance issues.

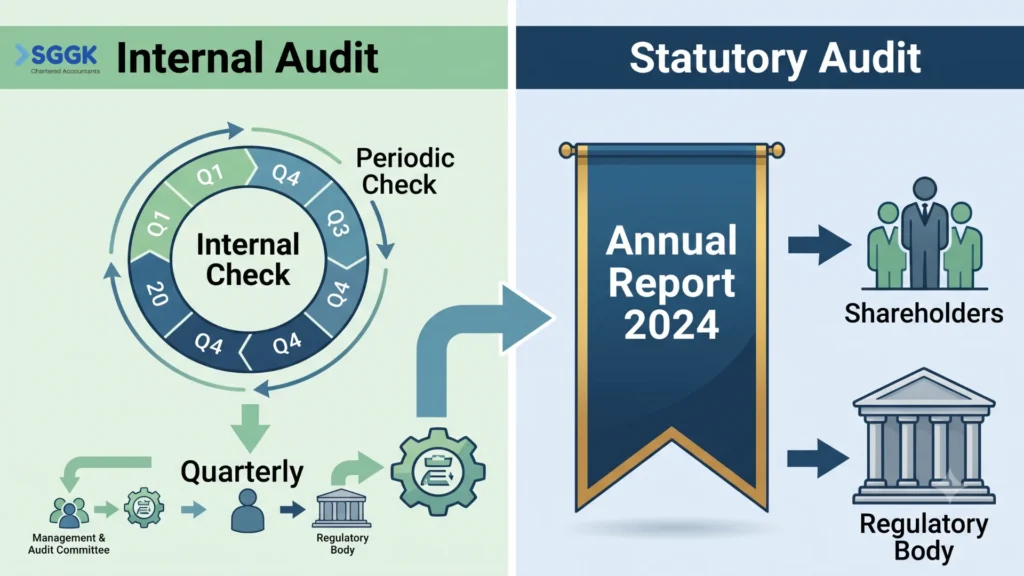

SGGK’s view of the Internal Audit function and external audit requirements is that it should operate on an ongoing basis throughout the year rather than being periodic. Thus helping the organizations to strengthen their internal control framework, mitigate risk, and enhance corporate governance.

Expert Insights: Growing companies often make the mistake of viewing audits as an annual compliance burden to check off. However, today’s good governance requires continuous oversight from stakeholders, such as investors, lenders, and regulators. Your internal audit serves as a steady navigation system to keep you heading in the right direction, while your statutory audit acts as an annual inspection of the overall functioning of your financial engine.

What Is an Internal Audit?

An internal audit sees how effectively the organization’s management evaluates its operations and controls. The internal auditor’s role is to identify weaknesses in the organization’s operations and controls that could lead to revenue loss or reduced productivity. They review whether operations and controls have been performed accurately, present suggestions for improving operational effectiveness, and prevent fraud.

Some primary objectives of internal auditing include:

- To manage or mitigate risk by identifying areas where the likelihood that an occurrence will become a substantial issue is high.

- To improve business processes by evaluating the effectiveness of the performance of business functions and to monitor the effectiveness of the management of the business functions.

- To evaluate if there are effective operational controls and whether such controls are being implemented appropriately.

- To identify any signs of possible fraud, errors, or other weaknesses in controls.

Who Conducts Internal Audits in India?

Under the 2013 Companies Act audit, many companies use the following methods to conduct an internal audit:

- An external chartered accounting firm was engaged to conduct internal audits.

- A cost accountant or other professional agreed to by the board of directors.

At SGGK, we offer CFOs and finance departments at growing firms a way to obtain their internal audit services through a CA firm when they don’t have sufficient internal resources or expertise to complete them.

The Institute of Internal Auditors (IIA) defines internal auditing as an independent assurance and consulting activity designed to improve the efficiency and effectiveness of an organization’s operations and to establish a better system for managing risk within that organization.

When Is Internal Audit Mandatory Under the Companies Act, 2013?

Section 138 of the Companies Act, 2013, read with Rule 13 of the Companies (Accounts) Rules, 2014, mandates internal audit for the following classes of companies.

Internal Auditing Requirements

There is a requirement for the appointment of an Internal Auditor within the following classes of companies:

Any listed company, irrespective of the business size.

All unlisted public companies that have either:

- Rs. 50 crores or more shares issued to the public.

- Achieved Rs. 200 crores or more in sales.

- Have over Rs. 100 crore owed to a bank or public institution.

- Has deposited Rs. 25 crore or more money with someone other than an institution.

Private companies have either achieved sales of Rs. 200 crore or more or owed money to a bank or public institution exceeding Rs. 100 crore.

If your company meets any one of these conditions, you must appoint an internal auditor.

Companies That Should Consider Internal Audit Even When Not Mandatory

Even when the law does not mandate that a business conduct internal auditing, it remains extremely useful for a variety of reasons.

- Many Venture-funded startups with Series A funding look for good practices and governance.

- Companies that are expanding very quickly face issues that require close attention to their rate of expansion.

- Multiple manufacturing locations make management more difficult and create a riskier environment.

- Private equity-backed companies will usually be required to provide internal audit reports in a format to the PE fund that owns their equity.

What Is a Statutory Audit?

When we compare internal audits vs. statutory audits, it is clear that Statutory audits examine a company’s financial records and verify the accuracy and fairness of its financial position. An independent auditor conducts statutory audits.

The Companies Act requires that a statutory auditor be appointed and that all companies under the Companies Act, 2013, both public and private, have their Financial Statements audited annually by an independent third party.

- Determine whether the financial records comply with generally accepted accounting principles and applicable laws.

- The Financial statements contain sufficient Information. The Financial Statements are Current.

- They analyze internal controls over financial reporting and issue an opinion on their effectiveness.

- After giving an opinion on the reliability of financial statements, the auditor shows shareholders, creditors, and regulators that they can fully rely on the Financial Statements.

Who Can Act as a Statutory Auditor in India?

Chartered Accountants registered with the Institute of Chartered Accountants of India (ICAI), or CA Firms registered with ICAI, can serve as statutory auditors.

All auditors will rotate after 5 years as an individual auditor and 10 years in CA Firms for the audit of listed companies.

Most of the company’s financial statements are reviewed by the statutory auditors. They also keep checking the accounting records that support the financial statements. The statutory auditor’s main aim is to establish whether the company’s financial statements are complete and legally compliant.

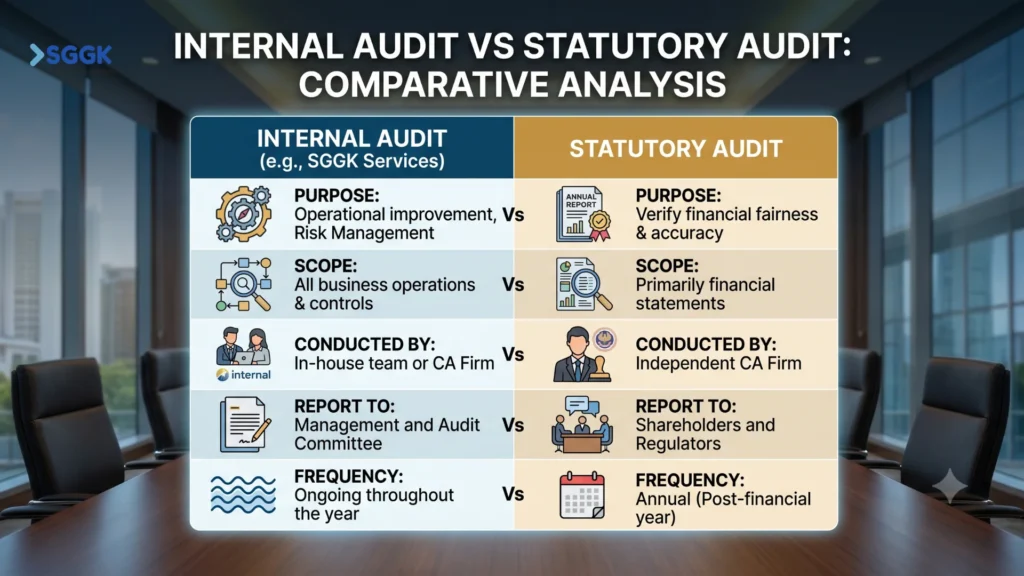

Internal Audit vs Statutory Audit: Comparison

Through this table, let’s understand internal audits vs external audits. With a comparative overview of their purposes, audit scopes, reporting structures, and roles.

Area | Internal Audit | Statutory Audit |

Purpose | To improve business processes, internal controls, and risk management. | To ensure the appropriateness of the financial statements. |

Scope of Audit | All business operations, including operational processes, IT systems, payroll, and inventory | Primarily based on financial statements and related disclosures |

Independence | Reports directly to management and the Audit Committee | Must maintain total audit independence from the entity being audited |

Reporting Structure | Reports are shared internally with management. | Reports are shared with shareholders and regulators. |

Regulatory Requirement | Mandatory only for specified companies under Section 138. | Mandatory for all companies under the Companies Act, 2013. |

Audit Methodology | Utilizes a flexible risk-based approach to the audit | Utilizes prescribed Standards on Auditing |

Risk Assessment | Assesses operational & compliance risks, IT risks, and fraud risk | Assesses risk of fraud and material misstatement |

Frequency & Timing | Conducted continuously per the audit plan | Conducted at least annually after the end of the financial year |

Deliverables | Internal Audit Report, including findings and recommendations | Auditor’s Report, CARO Report, Statutory audit reports |

Stakeholder Expectations | Improve management efficiency and governance | Assure Stakeholders regarding the reliability of financial information. |

Internal Audit and External Audit: How They Work Together?

Internal audit and external audit should not be regarded as substitute services by strong finance organizations. When used together, they support better governance, stronger control systems, and more reliable financial statements.

Internal Audit vs. External Audit: Why One Does Not Replace the Other

While understanding internal audits vs statutory audits in detail, it is clear that they serve completely different purposes.

Internal audits are intended to support continuous improvement across all areas of a business, from an operational standpoint, throughout the year.

Statutory audits, on the other hand, provide an opinion that the financial statements are free from material misstatements.

The objectives of each are clearly different; therefore, one cannot be substituted for the other. If your organization relies solely on a statutory audit, you could be late in identifying problems. In contrast, if you do not perform a statutory audit, you could be at high risk of failing to meet regulatory and legal obligations.

How Internal Audit Improves the Outcomes of Statutory Audits?

When executed effectively, the internal audit process supports the statutory audit process and enables greater efficiency.

By creating consistent documentation through internal audits, there will be less time spent gathering last-minute data for audits.

The SGGK statutory audit service in India works with developing organizations by providing audit support and regulatory compliance with external regulations.

Expert opinion: A common error made by developing companies is viewing audits as required and that they should occur only once each year to be compliant. However, growing stakeholder expectations for governance require organizations to maintain a consistent, enhanced oversight system across all components of governance.

An internal audit provides ongoing oversight to ensure that the organization is performing in accordance with established policies and procedures. A statutory audit provides independent verification of the organization’s final financial results following the completion of the audit.

Together, internal and statutory audits will provide an organization with a solid foundation for compliance and greater resilience.

Conclusion

Understanding the difference between Internal auditing and statutory auditing makes the audit process easier.

One of the leading causes of delays in the audit process is the absence of documentation or incomplete reconciliation or supporting documentation.

SGGK helps businesses prepare for audits by improving their financial processes and providing professional audit support services throughout the audit lifecycle.

If you are looking for a statutory auditor in India to transform your audits from a compliance maze into a strategic asset, contact SGGK to assist you with your audit needs.