How Audit Support Services Fix the Big 6 Readiness Gap?

Many companies enter a Big 6 audit believing they are well prepared, because their books are accurate and their financial reporting is up to date. Yet once fieldwork begins, they face a growing list of audit queries, documentation requests, and tight timelines. Audit Support Services for Big 6 are designed to prevent exactly this by preparing finance teams before fieldwork begins.

More often, finance teams are simply working with a different definition of “ready” than the one Big 4/Big 6 auditors use. Their documentation and control evidence are not necessarily wrong. They are simply built for a different audience.

We call this the Big 4/Big 6 readiness gap, and closing it isn’t about scrambling to answer queries faster. It means understanding the standards well enough to anticipate what auditors will ask before they ask it, and having someone coordinating that response from before day one of fieldwork. This is the work SGGK’s audit support engagements are built around.

Table of Contents

What Makes a Big 6 Audit Different?

| Aspect | Traditional Statutory Audit | Big 6 Audit |

|---|---|---|

| Documentation Standard | Prepared to adequately demonstrate compliance with applicable accounting and auditing standards. | Requires contemporaneous, comprehensive, evidence-driven documentation capturing procedures, professional judgments, discussions, and conclusions that can withstand reperformance and multiple review levels. |

| Review Process | Limited review levels with relatively straightforward supervision. | Multi-level internal review process involving seniors, managers, directors, and partners. |

| Audit Queries | Queries generally focus on obtaining sufficient information and evidence to support the audit opinion. | Queries are more extensive, risk-focused, and iterative, requiring detailed explanations, corroborative evidence, and documentation supporting management’s judgments. |

| Reporting Approach | Primarily focused on statutory reporting requirements and significant audit findings. | Reporting is more comprehensive, emphasising observations, root cause analysis, risk implications, recommendations, governance matters, and documentation of significant judgments. |

| Audit Timelines | More flexible timelines with greater scope for adjustments during the engagement. | Strict audit milestones with defined fieldwork schedules, review deadlines, and reporting timelines. |

In SGGK’s experience, the readiness gap rarely comes down to the finance team’s competence. It comes down to a mismatch in what “done” means.

A finance team closes its books when the numbers tie out. A Big 4/Big 6 reviewer considers the work done when the evidence trail behind those numbers can survive being handed to a stranger. Most companies only discover that gap in week two of fieldwork, when it is already expensive to close. Meeting Big 4/Big 6 compliance requirements means preparing for the second definition from day one, not the first.

Why Companies Struggle With Big 6 Audit Expectations?

Most finance teams are not short on effort. They are short on the specific muscle memory that a Big 4/Big 6 audit demands.

Documentation Gaps

Imagine being asked to explain a reconciliation six months after it was prepared with no prior context. That’s effectively the standard Big 4/Big 6 auditors work against.

Under Standard on Auditing (SA) 230, the auditor’s documentation must be detailed enough that an experienced auditor with no prior connection to the engagement can understand the work performed and the conclusions reached simply by reviewing the file.

That standard also shapes what auditors expect from the client: a clear trail of source data, workings, sign-offs, and a logical path from the trial balance to the financial statements. Internal teams often maintain records designed for management reporting rather than external audit evidence, and the two rarely match.

Timeline Pressure

Big 4/Big 6 firms run audits on a structured fieldwork calendar with defined milestones.

If your team is still assembling fixed asset schedules or debtor confirmations in week three, the audit does not wait. Delays on your side push queries into the final stretch, which is exactly when review pressure peaks on both sides.

Technical Knowledge Gaps

Disclosure requirements under Ind AS, CARO reporting, and internal financial control testing all carry a level of technical detail that goes beyond routine bookkeeping.

A finance controller who runs an excellent monthly close may still be unfamiliar with how a Big 4/Big 6 team documents control walkthroughs, or what evidence satisfies a test of design and a test of operating effectiveness under SA 500.

This is why many organisations supplement their internal finance teams with specialist audit support during the audit cycle, bringing in expertise that complements existing capabilities without disrupting day-to-day operations.

What Audit Support Services For Big 6 Actually Do ?

Audit Support Services in Bangalore for the Big 6 are not the same as a statutory. A statutory audit is performed by an independent auditor who reviews and forms an opinion on the financial statements. Audit support operates on the other side of that relationship, helping the company’s finance team prepare for the auditor, respond to the auditor, and close the audit without last-minute chaos.

In practice, this covers:

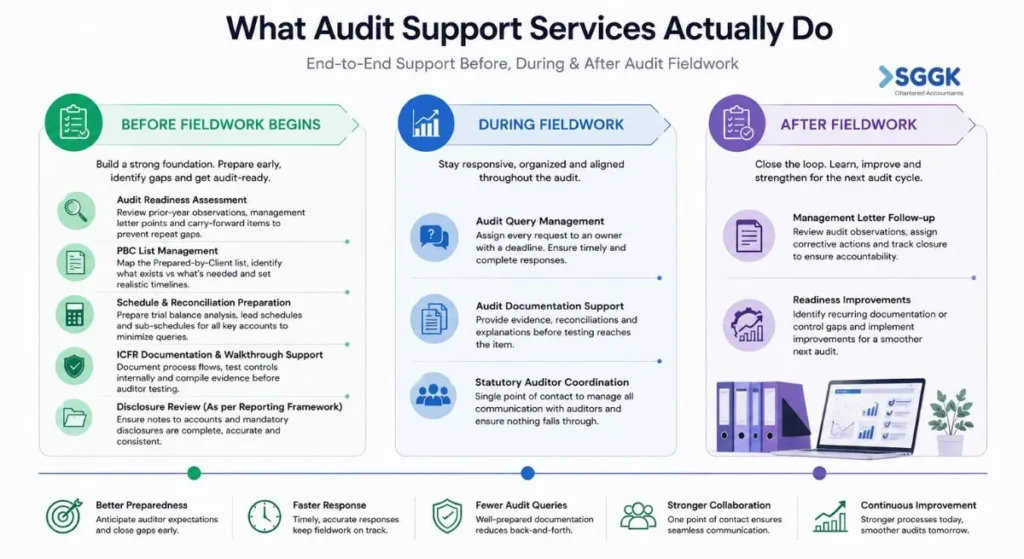

Before Fieldwork Begins

The foundation of a smooth audit is laid well before the auditors arrive. This phase emphasises the preparation of paperwork, the identification of gaps, and the assurance that the finance team is prepared for an audit.

- Audit readiness assessment: a structured review of prior-year audit observations, management letter points, and carry-forward items, done before the current cycle begins, so the same gap does not repeat itself for the third year running.

- PBC list management: working through the anticipated Prepared-by-Client list early, mapping what already exists against what needs to be built, and assigning realistic timelines instead of discovering the full scope only after the auditors have arrived.

- Schedule and reconciliation preparation: trial balance analysis, lead schedules, and sub-schedules across fixed assets, debtors, creditors, provisions, and bank reconciliations, prepared to a standard that does not generate a second round of queries for the same item.

- ICFR documentation and walkthrough support: process flows documented, controls tested internally, and evidence compiled before the auditors begin their own controls testing, rather than being built reactively when a control gap is flagged mid-fieldwork.

- Disclosure requirement as per reporting framework: reviewing the financial statements against the applicable disclosure checklist to ensure that the notes to accounts and other mandatory disclosures are complete, accurate, and consistent with the underlying financial records before the commencement of audit fieldwork.

During Fieldwork

Once fieldwork begins, speed becomes just as important as accuracy. Delayed responses often create additional review cycles, even when the underlying documentation is correct.

- Audit query management: Every request is assigned an owner and a deadline. Nothing sits unanswered long enough to slow down fieldwork.

- Audit documentation support: Evidence, reconciliations, and explanations are ready before testing reaches that item, not assembled after the auditor asks.

- Statutory auditor coordination: One point of contact manages all communication with the auditors. Requests do not get lost between departments or answered twice.

After Fieldwork

Audit support doesn’t stop after fieldwork is done. Post-audit observations assist in enhancing preparation for future audit cycles.

- Management letter follow-up: Review audit observations, assign corrective actions, and monitor closure.

- Readiness improvements: Identify recurring documentation or control gaps and implement improvements to make the next audit more efficient.

The Response Readiness Gap in Audit Support Services for Big 6

Two companies can walk into fieldwork with identical documentation and have completely different audit experiences because one team can articulate the reasoning behind a number on the spot, and the other cannot.

Big 6 auditors are not just verifying documents. They are testing whether the finance function itself understands the numbers it has produced.

A reconciliation without someone who can defend the judgement calls behind it, an estimate, a provision, a related party treatment, invites more scrutiny, not less. This is the response readiness layer, and it is the one most companies discover they are missing only after the auditor’s third follow-up question on the same item.

It is also why SGGK’s audit support is built to sit with the finance team well before fieldwork, rather than arrive as document-collection help once queries have already started. Preparation built in September for a March audit produces a fundamentally different fieldwork experience than preparation attempted in February.

A common audit readiness issue is treating IFC and ICFR as the same compliance requirement. IFC is a broader management responsibility under Section 134(5)(e) of the Companies Act, 2013, and it applies to every company regardless of size. ICFR is narrower: it is where the auditor forms and expresses an opinion on the adequacy and operating effectiveness of controls, governed under Section 143(3)(i), read with the Companies (Audit and Auditors) Rules, 2014, and it comes with specific applicability thresholds.

Why Audit Queries Keep Multiplying ?

Audit queries rarely multiply due to a single major issue. More often, they build on each other. One incomplete response leads to another request, then another reviewer asks a follow-up question, and suddenly a single reconciliation has generated five separate audit discussions.

- Many follow-up queries are typically due to incomplete schedules or lack of supporting materials.

- There is a greater requirement for further explanations due to ambiguous accounting decisions and lack of audit proof.

- Queries that go through manager and partner reviews need more specific documentation.

- Without a formalised method to monitor, allocate and address questions, finance teams often spend valuable time dealing with the same issues.

- With effective audit assistance, all queries are answered with well-substantiated replies, so there’s not too much back and forth and fieldwork stays on time.

The Hidden Cost of Poor Audit Readiness

The real cost of poor audit readiness rarely appears on the audit invoice. It appears in extended fieldwork, delayed financial reporting, repeated auditor interactions, and management time diverted from running the business. Most of these costs are preventable when readiness begins months before fieldwork rather than weeks before it.

A Practical Readiness Checklist for CFOs and Controllers

Before your next Big 4 fieldwork begins, it is worth testing your team against these questions:

- Are prior-year management letter points already closed, or still open?

- Does your team have a current, tested ICFR walkthrough document, or is it more than a year old?

- Is your PBC list mapped against existing documentation, with clear owners assigned?

- Can someone other than the CFO explain the reasoning behind your major estimates and provisions?

- Is there a single point of coordination for auditor queries, or does every query route through an already-stretched finance head?

If more than two of these answers are uncertain, the readiness gap already exists

How Audit Support Services for Big 6 Close the Audit Readiness Gap?

Understanding What Is Audit Readiness is the first step toward building documentation, controls, technical preparedness, and response readiness well before fieldwork begins. It is developed through consistent documentation practices, well-defined controls, technical preparedness, and the ability to respond confidently to auditor questions throughout the engagement. Organisations that embed these disciplines into their finance function are far more likely to experience efficient audits, fewer last-minute surprises, and stronger stakeholder confidence.

Ultimately, the difference between a stressful audit and a predictable one is rarely the quality of the accounting. More often, it is the quality of the preparation behind it. The same financial statements can lead to very different audit experiences depending on how well the underlying evidence, controls, and responses have been prepared.

At SGGK, our Audit Support Services for Big 6 help finance teams build Documentation Readiness, Control Readiness, Technical Readiness, and Response Readiness well before auditors arrive. By addressing these four layers early, organisations can reduce avoidable audit queries, improve collaboration with auditors, and approach Big 6 audits with greater confidence and control.

Prepare for Your Next Big 6 Audit with Confidence

FAQs Related To Audit Support Services for Big 6

What is the difference between a statutory audit and audit support services?

A statutory audit is performed by an independent auditor who examines the financial statements and forms an opinion. Audit support services sit on the client's side of that process. They help the finance team get documentation ready, answer queries, and manage day-to-day communication with the engagement team. The opinion itself is still the statutory auditor's to give.

When should a company start Big 6 audit readiness work??

Ideally, months before fieldwork begins, not weeks. Readiness that starts after the prior year's management letter points are reviewed gives the finance team time to close gaps instead of reacting to them during fieldwork.

Is Big 6 audit support only for large companies?

No, Company size doesn't change what a Big 6 auditor expects. The documentation standard, the review layers, and the disclosure requirements stay the same whether the finance team has 50 people or five